Options Trading Strategies: Put Backspread

A put backspread (otherwise called a ratio volatility spread with puts and put ratio backspread) is a three-legged strategy, created by buying two Out of The Money puts and selling one In The Money (or At The Money) put. All puts are with the same expiration date.

A 2:1 put ratio backspread can also be created by selling a number of ITM (or ATM) puts and buying twice the number OTM of puts.

You can look at a put backspread as a combination of a bull put spread and one OTM long put.

When to use this strategy?

You are extremely bearish and looking for a low risk, low-cost trade, and the volatility of the BTC/ETH is really high.

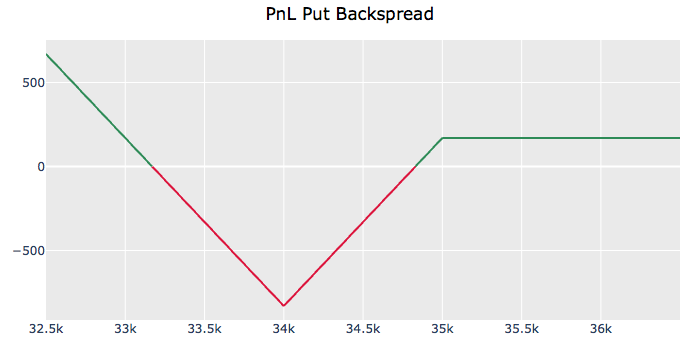

Below is a Profit and Loss chart example of a put backspread options strategy:

Pros:

Capped risk, especially if the BTC/ETH rises drastically. Uncapped and high reward if the BTC/ETH price drops drastically.

Cons:

Relatively complicated trade for beginners. High loss if the underlying price stagnates.

Example:

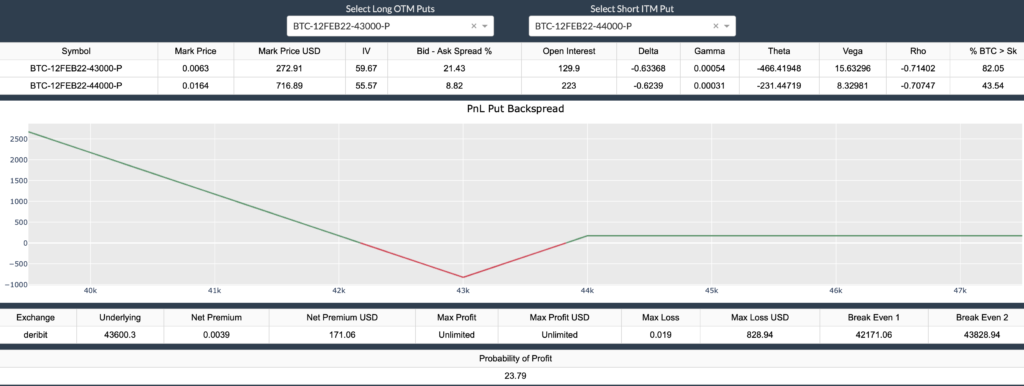

In this example, BTC is trading at 43,600.30 USD, and you expect its price to dramatically move, preferably fall. You have bought two OTM puts with a strike price of 43,000.00 USD, and sold an ITM put with a strike price of 44,000.00 USD, all with an expiration date of February 12th 2022.

As this is a net credit spread, and the long puts cost you less than a premium from the short put, you have received a net premium of 171.06 USD.

The Profit and Loss chart is given below:

Upon expiration:

If the BTC price is below the OTM long puts strike price, then the short put is assigned and both long puts are exercised, so you are in the profit as long as the bitcoin price ends up below the first break-even point.

If the BTC price is equal to the OTM long puts strike, you are at your maximum loss which is equal to the difference between strikes minus the net premium.

If the BTC price is above the OTM long puts strike and below the ITM short put strike, then the short put is assigned and the long puts expire, so you are in the profit as long as the bitcoin price ends up above the second break-even point.

If the BTC price is at or above the strike price of the ITM short put, then all options expire worthless, and you get to keep the net premium.

| BTC at Expiry (USD) | Payoff (USD) |

|---|---|

| 40,012.00 | +2,159.06 |

| 41,132.00 | +1,039.06 |

| 42,171.06 (break even 1) | 0 |

| 42,644.00 | -472.94 |

| 43,000.00 (2 x LP OTM) | -828.94 (max loss) |

| 43,454.00 | -374.94 |

| 43,820.94 (break even 2) | 0 |

| 43,917.00 | +88.06 |

| 44,000.00 (strike price SP ITM) | +171.06 (net premium) |