Options Trading Strategies: Short Straddle

The short straddle (otherwise called a sell straddle or a naked straddle sale) is a two-legged strategy, created by selling one At The Money call and selling one At The Money put, both with the same expiration date and a strike price.

When to use this strategy?

You are extremely bearish on the volatility and convinced that in the selected time frame the underlying price will stay unchanged, and you are looking for a direction neutral income strategy.

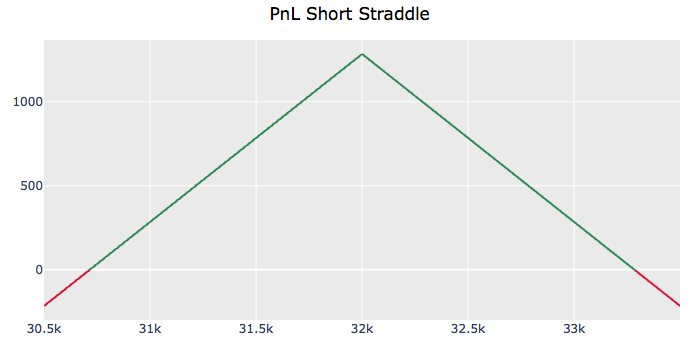

Below is a Profit and Loss chart example of a short straddle options strategy:

Pros:

Can be a high return income strategy if the underlying price stagnates.

Cons:

High and uncapped risk, capped maximum profit.

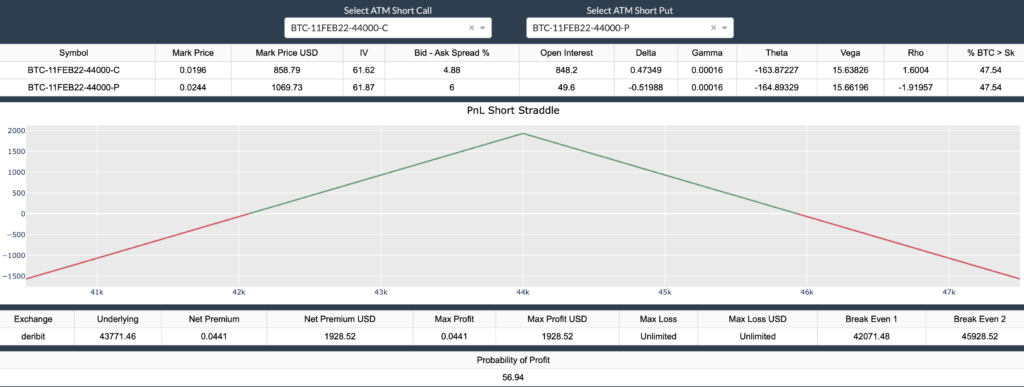

Example:

In this example, BTC is trading at 43,771.46 USD, and you expect its price to stagnate. You have sold an ATMcall and an ATM put both with a strike price of 44,000.00 USD, with an expiration date of February 11th 2022.

As this is a net credit spread you have received a net premium of 1,928.52 USD which is also your maximum profit.

Upon expiration:

If the BTC price is below the strike price, the short call expires worthless and the short put is assigned, you are in the profit as long as the bitcoin price ends up above the first break-even point.

If the BTC price is at the strike price, then both the call and the put expire worthless, and this is your maximum profit.

If the BTC price is above the strike price, the put expires worthless, the short call is assigned, you are in the profit as long as the bitcoin price ends up below the second break-even point.

| BTC at Expiry (USD) | Payoff (USD) |

|---|---|

| 40,878.00 | -1,193.48 |

| 41,718.00 | -353.48 |

| 42,071.48 (break even 1) | 0 |

| 43,031.00 | +959.52 |

| 44,000.00 (SC x SP ATM) | +1,928.52 (max profit) |

| 44,896.00 | +1,032.52 |

| 45,928.52 (break even 2) | 0 |

| 46,397.00 | -468.48 |

| 47,034.00 | -1,105.48 |